Unseen Inflection: Soil Gene Editing as a Wildcard Reshaping Biotechnology’s Industrial and Regulatory Landscape

An emerging under-recognized development in synthetic biology and biotechnology is the progressive regulatory openness and innovation focus on soil and plant gene editing in Europe and beyond. This signal could plausibly catalyze a structural shift in capital flows, regulatory frameworks, and agricultural-industrial integration over the next decade.

Recent activities spotlight an evolving pivot towards gene editing technologies applied to soil health and agriculture, enabled by genome-editing tools like CRISPR and emerging techniques such as phage-assisted continuous evolution (PACE). Unlike conventional transgenics, these approaches intersect complex ecosystems and biomes, activating new debates about regulation, liability, and industrial strategy. This signals a possible inflection point where biotechnology’s domain expands from discrete therapeutic or industrial applications into foundational enhancements of terrestrial ecosystems.

Signal Identification

This development qualifies as an emerging inflection indicator due to its dual technological and regulatory novelties that challenge incumbent governance and investment paradigms. It is anchored in evolving gene editing techniques (e.g., CRISPR, PACE), coupled with a nascent acceptance of gene-editing for plants and soil microbiomes, especially within the EU and UK, regions historically risk-averse toward genetically modified crops (AgTech Navigator 19/01/2026; European Commission 22/03/2026). The plausibility horizon spans medium term (~5–10 years), with a high plausibility band given current policy signals and advancing technology readiness. Key impacted sectors include agricultural biotechnology, industrial biotechnology, environmental management, specialty biopharmaceuticals (considering microbiome therapies), and regulatory governance.

What Is Changing

At a technological level, precision genome editing via CRISPR and promising supplemental techniques like PACE are overcoming prior bottlenecks in modifying complex organisms, including soil microbiomes and plant species with finely tuned traits. The capacity to edit soil health—by modulating microbiomes, nutrient cycles, or plant-soil interactions—represents a foundational expansion of synthetic biology’s domain beyond isolated gene therapies and microbial industrial fermentations (Harvard Gazette 14/05/2026; PMC NCBI 08/03/2026).

Regulatory stances are shifting in parallel, with the EU and UK signalling a more permissive approach to gene editing for plants and microbiomes, diverging from their conservative genetic modification (GM) policies from prior decades. This regulatory openness, coupled with the European Commission’s drive to position the EU as a global biotechnology innovation leader, creates fertile conditions for capital formation and ecosystem development in soil and agricultural biotech (European Commission 22/03/2026; AgTech Navigator 19/01/2026).

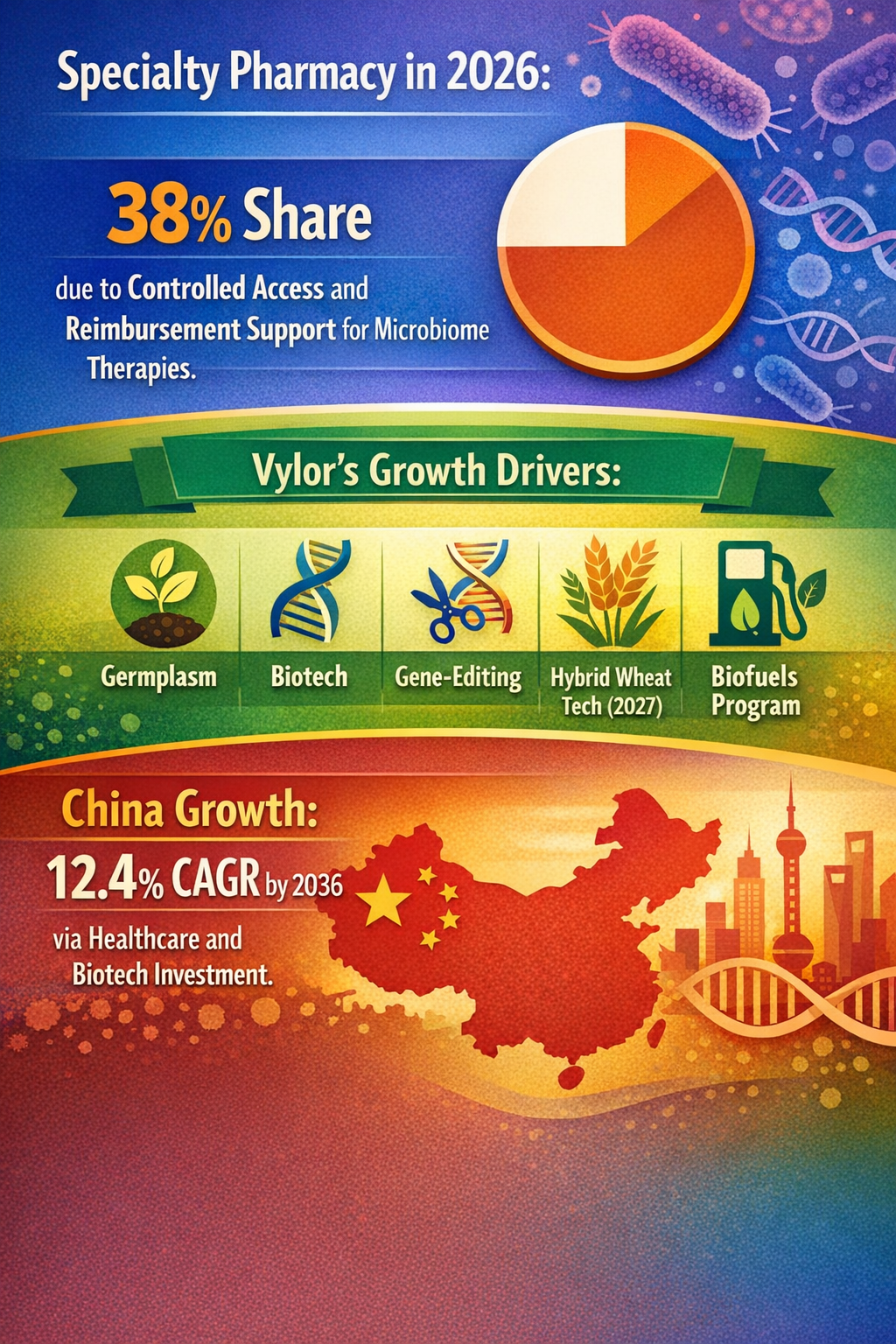

Another structural evolution involves the intersection with microbiome therapeutics. The emerging specialty pharmacy channel for microbiome therapies—which are expected to hold a 38% share of that market by 2026—may increasingly interface with agricultural and environmental applications via cross-sectoral biotech platforms. This hints at convergence between human health, environmental biotech, and agriculture, expanding the synthetic biology value chain beyond traditional silos (FactMR 15/02/2026).

What is genuinely novel is the potential systemic scale of impact: rather than incremental improvements, editing ecosystem-level functions in soil could disrupt agricultural supply chains, regulatory jurisdictions, capital allocation priorities, and industrial collaboration models. This is an under-recognized structural inflection, distinct from well-covered genome editing in human therapeutics or industrial enzymes. It involves a multi-stakeholder, multi-scale challenge bridging ecosystem services, climate resilience, and bioeconomy governance.

Disruption Pathway

The pathway begins with further maturity and cost reduction of precision gene editing technologies for soil and plant microbiomes, enabling diverse trait development (e.g., drought tolerance, nitrogen fixation enhancement, disease resistance). Continued R&D and pilot deployments could rapidly generate data sets demonstrating efficacy and safety, which may encourage regulators to codify new framework exemptions or fast tracks reflecting low-risk profiles of gene editing versus classical GM approaches (Harvard Gazette 14/05/2026).

As gene-edited products scale, agricultural supply chains might face stresses due to liability ambiguities arising from dispersed environmental releases of edited microbes and plants, challenging existing national and international regulatory harmonization focused on contained products. Commercial actors may respond by vertically integrating microbiome and gene-editing capacities with seed companies, environmental asset managers, and agricultural services firms, reflecting a consolidation dynamic across polycultures and crop protection industries (AgTech Navigator 19/01/2026).

Feedback loops could emerge where successful deployments incentivize further gene editing for ecosystem services—potentially reducing agricultural chemical inputs and generating carbon sequestration credits. This would realign capital allocation towards biotech-enabled sustainability outcomes, influencing public funding priorities and private investment trends within the EU and globally (European Commission 22/03/2026).

Under conditions of this acceleration, dominant regulatory models based on strict gene-editing containment and heterogeneous GM classifications may shift towards agile, risk-tiered regulatory frameworks prioritizing function over method. This could also redefine global trade compliance regimes as countries adopt divergent approaches to gene-edited crop and soil products, influencing strategic positioning among agricultural exporters and biotechnology firms.

Why This Matters

For capital allocators, this emergent signal may dictate a strategic reevaluation of risk and opportunity in agri-biotech ventures. Investments previously directed exclusively into plant breeding, pesticide development, or microbial industrial enzymes could shift toward integrated gene editing systems targeting soil ecosystems—potentially redefining portfolio benchmarks and VC investment theses.

Regulators face a complex challenge balancing innovation facilitation with precaution regarding unanticipated ecological impacts. The lack of harmonized global policy specifically addressing in situ gene editing of soil microbiomes introduces liability and compliance risks for multinational firms, while providing regulatory arbitrage opportunities.

Industrial actors—seed companies, chemical firms, microbiome startups, and agricultural service providers—may need to embed gene-editing capabilities and regulatory navigation expertise to maintain competitive positioning, risking disintermediation or obsolescence otherwise. Supply chain ramifications include potential shifts in input sourcing, crop insurance, and environmental credit markets.

Governments and multilateral bodies might confront governance dilemmas over transboundary impacts, environmental monitoring, and public trust management as gene-edited microbiomes could diffuse beyond original release zones.

Implications

This development could likely catalyse a multi-decade replatforming of bioscience applications into foundational ecosystem management. Capital flows may realign heavily toward integrated ag-bio ecosystems, fostering emergence of new industrial champions. Regulatory regimes might evolve from method-based prohibitions toward outcome-based risk assessments, impacting compliance costs and market access.

Transient or localized gene-editing projects focused on single crops or therapeutic targets should not be conflated with the systemic transformation potential of soil microbiome editing. Competing interpretations might downplay ecosystem risks or speculate excessively about gene drive scenarios; however, the most probable structural impact lies in politicized regulatory evolution and supply chain reorganization.

Early Indicators to Monitor

- Patent filings and publications on soil microbiome editing and PACE-related gene-editing technologies.

- Regulatory draft policies clarifying gene editing classification for plants and environmental applications, especially within EU/UK frameworks.

- Venture capital syndicates and corporate partnerships focused on integrated plant-soil biotech platforms.

- Capital reallocations from agrochemical firms toward gene-editing startups or environmental biotech funds.

- Contracts or procurement shifts by governments or multinational agribusinesses toward gene-edited crop and soil health innovations.

Disconfirming Signals

- Reversal or hardening of European gene editing regulations restricting environmental application beyond contained trials.

- Major field trial failures demonstrating ecological or agronomic instability of gene-edited soil microbiomes.

- Divergent global regulatory fragmentation leading to market inaccessibility for gene-edited agbio products.

- Emergence of superior alternative technologies (e.g., chemical, mechanical, conventional breeding) outpacing gene editing in cost and efficacy.

- Capitulation by major agri-industry incumbents to conservative R&D models avoiding gene editing innovations.

Strategic Questions

- How should capital allocation strategies be adapted to capture opportunities and manage risks from gene editing in ecosystem-level biotechnology?

- What regulatory frameworks can balance innovation incentives with environmental safeguards in gene-edited soil microbiomes?

Keywords

Gene Editing; Synthetic Biology; Soil Microbiome; Regulatory Frameworks; Biotechnology Investment; Agricultural Biotechnology; Phage-Assisted Continuous Evolution (PACE); Microbiome Therapeutics

Bibliography

- The European Commission aims to position the EU as a leader in biotechnology by advancing R&D, fostering an ecosystem where biotech innovation can thrive and boosting the growth potential of biotech companies in the EU. European Commission. Published 22/03/2026.

- By Sales Channel: Specialty pharmacy is projected to hold 38.0% share in 2026 as approved microbiome therapies require controlled access and reimbursement support. FactMR. Published 15/02/2026.

- Additionally, the discovery of genome-editing technologies such as Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR) has also opened up new avenues for India's biotechnology sector with the potential of bypassing some controversies associated with conventional transgenic methods. PMC NCBI. Published 08/03/2026.

- Soil health innovation more broadly will accelerate, particularly as Europe and the UK show increased openness toward gene editing in plants. AgTech Navigator. Published 19/01/2026.

- PACE could help solve a long-standing problem with gene editing. Harvard Gazette. Published 14/05/2026.