The Silent Inflection in Tokenised & Decentralised Finance: The Embedded Risks of Programmable Sovereign Debt

Programmable tokens representing sovereign debt—particularly dollar stablecoins backed by US Treasuries—may trigger fundamental shifts in global capital flows, regulatory frameworks, and monetary sovereignty within the next two decades. This emerging mechanism is insufficiently scrutinized as a systemic risk vector and a transformative factor in fiscal-monetary interaction.

Tokenisation of real-world assets is maturing rapidly, promising seamless tradability and programmability of physical and financial instruments. While regulatory advances in the US (GENIUS Act), Europe (MiCA), and pilot Central Bank Digital Currencies (CBDCs) are stabilizing the digital asset ecosystem, the intersection of fiscal policy and programmable digital stablecoins issued against sovereign debt poses a subtly disruptive force with far-reaching implications. This paper highlights the under-recognised weak signal of programmable sovereign debt tokens and delineates its potential to reshape capital allocation patterns, regulatory jurisdiction, and state financial resilience.

Signal Identification

The development of sovereign debt-backed programmable stablecoins qualifies as a weak signal with a medium-high plausibility of scaling into a structural inflection within 10–20 years. It is underappreciated because the dominant discourse focuses either on DeFi innovation or on regulation of general tokenisation without connecting these trends to sovereign fiscal strategies embedded in token design.

Exposed sectors include public finance, capital markets, monetary authorities, DeFi platforms, and international regulatory bodies. This signal reveals an emergent mechanism by which state fiscal operations and capital markets may be partially coded into programmable digital tokens, potentially altering leverage, market liquidity, and systemic financial risk.

What Is Changing

Asset tokenisation has evolved from a nascent concept to a mainstream expectation of how future finance will operate, with physical and financial assets increasingly represented as programmable, tradable digital units (KuCoin 30/03/2026). This tokenisation trend extends beyond private assets to include sovereign liabilities, particularly through dollar stablecoins that are essentially digitised US Treasuries (Business of Payments 10/05/2026).

At the regulatory level, frameworks like the US GENIUS Act and Europe’s Markets in Crypto-Assets (MiCA) regulation have de-risked the issuance of digital assets, paving the way for institutional capital to flow into these tokenised instruments (Kavout Market Lens 01/04/2026). This formalisation not only legitimizes but incentivizes the embedding of sovereign debt tokens into wider financial applications, including decentralised finance (DeFi) ecosystems.

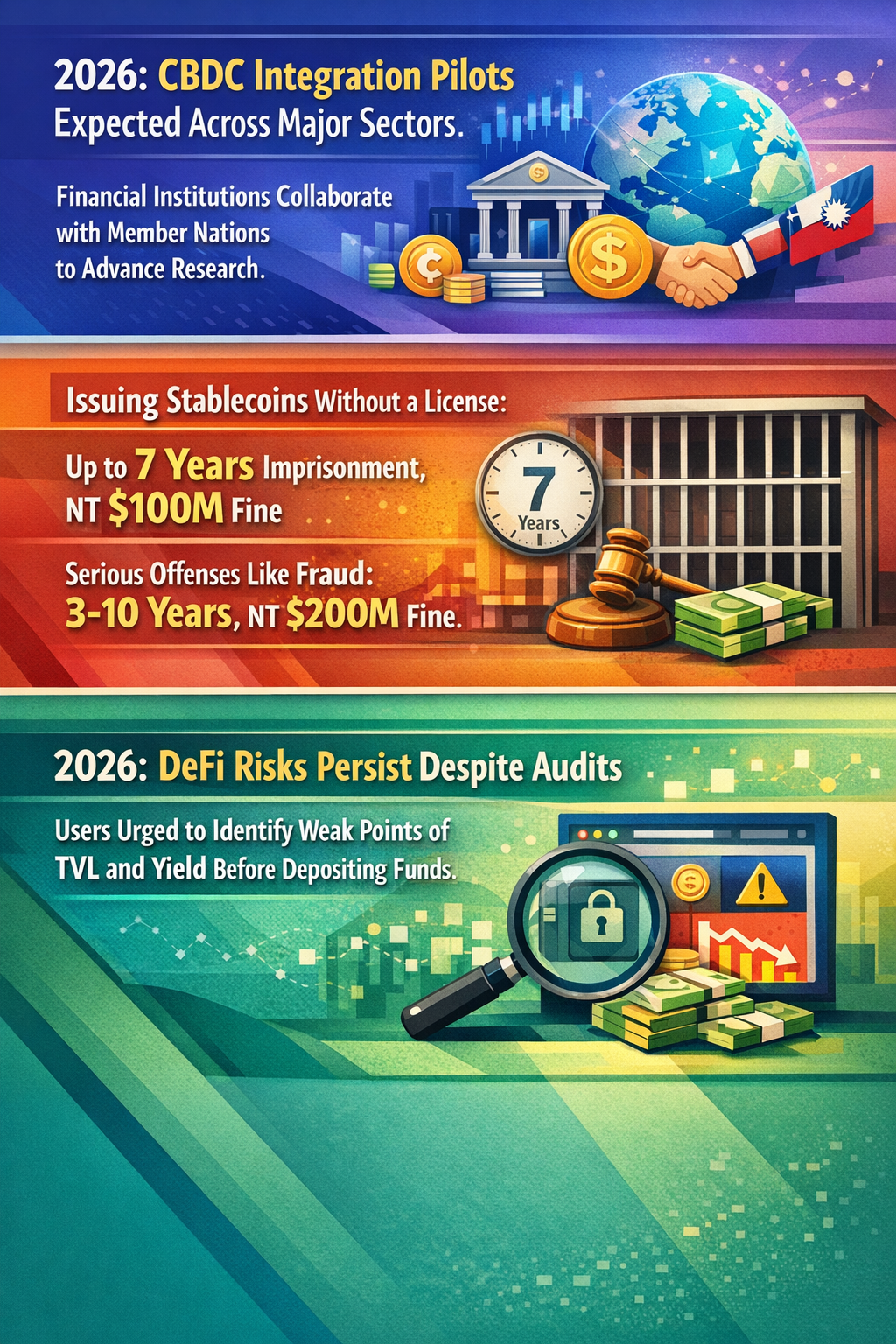

Meanwhile, governments anticipate Central Bank Digital Currencies (CBDCs) to integrate with tokenised financial ecosystems by 2026, indicating that state instruments will increasingly operate within programmable money networks (InfoBRICS 12/04/2026). However, the intersection of programmable sovereign debt tokens issuer-by-issuer, with their uniquely coded fiscal features—such as automated yield, on-chain compliance, and programmable redemption—introduces a substantively new dimension to public finance management and capital allocation.

Notably, US political actors are actively supporting dollar stablecoins linked directly to US Treasuries as a means to sustain large fiscal deficits efficiently (Business of Payments 10/05/2026). This pivot suggests a future where fiscal operations are embedded into digital programmable layers, enabling unprecedented traceability and execution speeds but also exposing public finance to novel systemic risks hitherto under-explored.

Disruption Pathway

As programmable sovereign debt tokens scale, liquidity dynamics in sovereign debt markets may shift. The automated, programmable nature of tokens allows holders to execute complex financial strategies instantaneously via smart contracts, potentially increasing volatility and leverage beyond current oversight capabilities.

The acceleration conditions include further regulatory clarity (e.g., broader adoption of frameworks like the GENIUS Act), technological maturity in blockchain infrastructure, and growing institutional participation in tokenised assets as safer alternatives to conventional fiscal instruments. Regulatory de-risking may paradoxically speed issuance by lowering entry barriers to issuing programmable debt tokens.

This creates stress on existing capital market architectures and monetary control mechanisms. For instance, the US Treasury market has historically been a pillar of global financial stability; a programmable token overlay could fragment liquidity, complicate monetary policy transmission, and heighten cross-border regulatory arbitrage.

Structural adaptations may involve the emergence of hybrid supervisory regimes integrating traditional fiscal authorities, securities regulators, and digital asset oversight bodies. Furthermore, new market infrastructures specializing in token custody, audit, and stress-testing programmable sovereign debt will evolve. These infrastructures must address previously unquantifiable DeFi risks such as smart contract vulnerabilities in mission-critical sovereign tokens (CryptoSlate 22/03/2026).

Feedback loops could arise if programmable debt tokens enable faster capital reallocation in and out of sovereign credit, amplifying yield spikes and liquidity droughts. This could force central banks to reconsider quantitative easing tools and debt monetization channels.

Dominant regulatory models might shift towards integrated fiscal-monetary control frameworks that intervene directly in programmable digital asset issuance to preserve economic stability, potentially imposing licensing regimes with criminal penalties as severe as those highlighted in anti-money laundering frameworks (Zigram Tech 06/04/2026).

Why This Matters

Decision-makers in capital allocation, fiscal policy design, and financial regulation must recognize programmable sovereign debt tokens as both opportunities for enhanced efficiency and controls, and as vectors for systemic risk.

Capital exposure risks shift as institutional investors may increase allocation to programmable sovereign tokens expecting enhanced liquidity and yield programmability, unaware of embedded digital risk. Regulators face complex jurisdictional challenges in supervising programmable assets that can dynamically alter state financial exposure.

Governments may experience a recalibration of fiscal sovereignty if programmable debt tokens redistribute capital flows rapidly across borders and via DeFi channels, limiting conventional policy instruments’ effectiveness. This redistribution may also reshape industrial structures by incentivizing new fintech platforms that integrate programmable sovereign instruments.

Liability frameworks must evolve to encompass risks of smart contract failure, fraud, or manipulation embedded within sovereign debt tokens, demanding new legal and compliance infrastructures.

Implications

The widespread adoption of programmable sovereign debt tokens could likely transform global capital market functioning and public finance resilience over the next two decades. Governments might achieve more agile fiscal management but could simultaneously lose some control over debt servicing dynamics and monetary policy implementation.

This development is not a mere incremental improvement of current digital asset technologies but a substantive structural alteration in how sovereign financing and regulatory governance are conducted.

Competing interpretations exist: some argue programmable sovereign tokens could democratize and stabilize fiscal markets, while others warn of exacerbated systemic risk and fiscal opacity.

Still, this signal is distinct from the more visible and hyped trends of retail DeFi growth or NFT market expansion; it focuses on embedded state instruments and their disruptive systemic potential.

Early Indicators to Monitor

- Regulatory developments expanding licensing for sovereign debt-backed stablecoins beyond the US GENIUS Act (Kavout Market Lens 01/04/2026).

- Issuer announcements of tokenised sovereign debt products with programmable yield or redemption features.

- Institutional capital reallocating from traditional sovereign bond ETFs into programmable sovereign tokens.

- Legal cases or regulatory penalties tied to programmable sovereign token misuse or fraud (Zigram Tech 06/04/2026).

- Emergence of specialized custodial or audit services focused on programmable sovereign instruments.

Disconfirming Signals

- Significant rollback or delaying of stablecoin regulatory frameworks, undermining token issuance legality.

- Technological setbacks or security breaches in programmable debt token smart contracts causing market rejection.

- Sustained preference by institutional investors for traditional sovereign debt channels due to risk aversion or regulatory opacity.

- Central bank rejection of CBDC and programmable token integration strategies (InfoBRICS 12/04/2026).

Strategic Questions

- How can regulators balance incentivizing programmable sovereign debt innovation with mitigating systemic financial risks?

- What contingency frameworks should governments develop to manage liquidity and monetary control risks arising from programmable sovereign tokens?

Keywords

Tokenisation; Programmable Finance; Sovereign Debt; Stablecoins; GENIUS Act; Decentralised Finance; CBDC; Financial Regulation

Bibliography

- As asset tokenization matures, it will likely become the standard operating layer for all global finance, turning every physical and financial asset into a programmable, tradable unit of the digital economy. KuCoin. Published 30/03/2026.

- Some in the US administration hope that explosive growth in dollar stablecoins - essentially tokenised US Treasuries - will allow it to continue running large fiscal deficits. Business of Payments. Published 10/05/2026.

- Regulatory frameworks, particularly the U.S. GENIUS Act and Europe’s MiCA, have significantly de-risked digital assets, paving the way for broader adoption and institutional capital inflows. Kavout Market Lens. Published 01/04/2026.

- Issuing stablecoins without a license could result in up to seven years in prison and fines of NT $100 million, while more serious offences such as fraud, concealment, or price manipulation could lead to 3-10 years imprisonment and fines up to NT $200 million. Zigram Tech. Published 06/04/2026.

- Member nations advance CBDC integration research right now, with financial institutions expecting pilot programs by 2026 across various major sectors. InfoBRICS. Published 12/04/2026.

- Audits, TVL, and yield still miss key DeFi risks in 2026, forcing users to ask what can break before they deposit funds. CryptoSlate. Published 22/03/2026.