Oral GLP-1 Weight-Loss Pills: The Under-Recognized Inflection in Diet Drug Structural Dynamics

Oral glucagon-like peptide-1 (GLP-1) receptor agonists for weight management signal a profound, underappreciated shift with potential to reshape pharmaceutical strategy, regulatory frameworks, and competitive landscapes over the next decade. While injectables have dominated obesity treatment, the convenience and evolving safety profile of oral formulations may accelerate patient adoption and induce systemic realignments.

The emerging inflection centers on oral GLP-1s stepping beyond incremental innovation into an enabler for sustained weight management adherence and expanded patient reach. This development, coupled with pending regulatory and reimbursement uncertainties, could disrupt capital flows, challenge incumbent pricing power, and redefine market structures within obesity and diabetes therapeutics.

Signal Identification

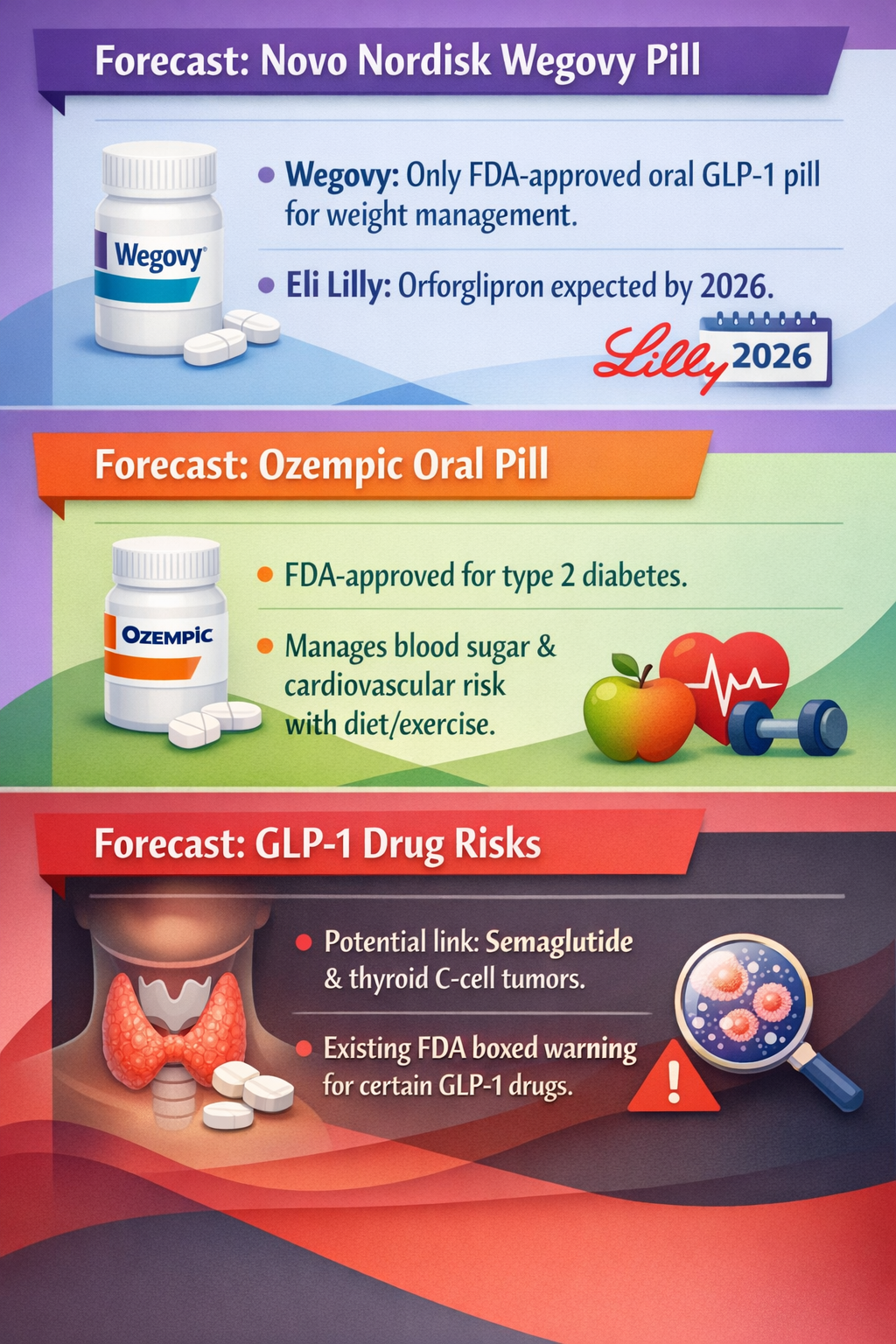

This development qualifies as an emerging inflection indicator. Oral GLP-1s represent a departure from decades of largely injectable weight-loss therapies by radically improving usability and potentially broadening patient adherence. The signal is medium-to-high plausibility given ongoing FDA approvals (e.g., Novo Nordisk’s Ozempic oral pill), pending pipeline launches (Lilly’s orforglipron in 2026), and rising clinical data addressing long-term weight loss maintenance (Fierce Pharma 11/05/2023; Pharmaceutical Technology 15/08/2023). Time horizon sits at 5–10 years for broad structural impacts as oral forms gain market share and reimbursement clarity. Affected sectors include pharmaceuticals, health insurance, clinical care delivery, and risk management.

What Is Changing

Multiple sources converge on the theme that oral GLP-1 therapies are shifting the obesity treatment paradigm from specialist-administered injectables to patient-friendly, at-home oral regimens. Novo Nordisk’s Ozempic oral pill approval marks a regulatory milestone, extending GLP-1 indications beyond type 2 diabetes into weight management with enhanced convenience (Pharmaceutical Technology 15/08/2023).

Lilly’s advancing pipeline attempts to close the gap with novel oral GLP-1 candidates aiming for similar or better efficacy and safety profiles, with expectations to launch orforglipron by 2026 (Forbes 31/03/2026). This introduces patient choice diversity and intensifies competitive positioning around oral delivery platforms.

Additionally, corporate communications about long-term weight loss maintenance data suggest oral GLP-1s could function beyond short-term management, raising expectations for chronic treatment adherence and more durable health outcomes (Fierce Pharma 11/05/2023). This is a key shift from episodic use patterns characteristic of earlier agents and injectables.

Notably, the emerging risk profile—such as signals linking Wegovy (injectable GLP-1) to ischemic optic neuropathy (ION)—suggests oral formulations may also influence risk-benefit assessments, impacting regulatory scrutiny and liability structures (Live Science 23/02/2024). Meanwhile, generic Ozempic approvals in jurisdictions like Canada introduce pricing pressure imperiling incumbent pricing power (Investing.com 12/12/2023).

Regulatory uncertainty remains pivotal—Medicare coverage for GLP-1s has no clear path beyond 2027 absent policy extensions or implementation of models like BALANCE, impacting payer risk calculus and access dynamics (KFF 02/04/2024).

Disruption Pathway

The pathway begins as oral GLP-1s overcome patient adherence barriers inherent in injectable regimes, attracting larger patient populations with obesity or diabetes, which remains under-treated due to convenience and stigma factors. Progressive clinical data affirming long-term maintenance potential amplify willingness among prescribers and insurers to endorse chronic use.

Simultaneously, oral formulations enable hybrid delivery models blending pharmacy dispensation and telemedicine, stressing traditional clinical pathways and counseling. This shift introduces new intermediaries and redefines point-of-care roles.

Cost dynamics evolve with generic oral GLP-1s entering select markets, forcing incumbent firms to reconsider premium pricing and expand volume-based approaches or diversify into vertically integrated care models. The erosion of pricing power stimulates R&D investments in differentiated molecules or adjunctive therapies.

Regulatory frameworks may adapt from siloed single-drug approvals towards integrated reimbursement packages considering patient adherence data and real-world outcomes, especially if experimental models like Medicare’s BALANCE demonstrate cost-effectiveness. This regime shift could precipitate more rigorous post-market surveillance capturing safety endpoints specific to chronic therapy, including rare adverse events like ION that emerged for Wegovy.

Feedback loops extend as expanded access and adherence data spur further public health initiatives targeting obesity, potentially repositioning GLP-1s from specialty drugs to mainstream care staples, with implications for global health systems and related supply chains.

Liability exposure might shift, as oral safety profiles and recorded adverse events call for updated pharmacovigilance and patient monitoring protocols, driving insurers and manufacturers to refine risk governance models.

Why This Matters

Capital allocation strategies must account for the disruptive potential of oral GLP-1s to redraw obesity and diabetes treatment market boundaries. Investment in pharmaceutical R&D pipelines, manufacturing capacities targeted at oral formulations, and distribution channels designed for broader patient reach may gain priority.

Regulators face pressure to devise more adaptive, evidence-based frameworks that incorporate adherence data and balance cost-benefit analyses over chronic treatment durations. Policymakers may need to address reimbursement volatility to ensure sustained patient access post-2027 Medicare bridge periods.

Competitive positioning will hinge on developing oral delivery innovations, managing generics threats, and navigating safety and liability landscapes, possibly prompting mergers or alliances between specialty drug developers and technology firms focused on digital adherence solutions.

Supply chains could see reshuffling as oral drugs can leverage existing oral pharmaceutical manufacturing infrastructure differently than injectables, impacting raw material procurement and finished product logistics.

Governance implications arise from evolving patient safety surveillance needs and payer frameworks, challenging public health bodies to integrate novel data streams and preventive care paradigms.

Implications

This emerging inflection is likely to initiate a structural rebalancing rather than transient market noise. Oral GLP-1s could become foundational pillars in weight management therapy paradigms within 5–10 years, eroding traditional reliance on injectable monopolies.

Capital markets may reallocate towards oral drug innovators and complementary digital adherence platforms, influencing M&A and venture flows.

Regulatory bodies might pivot from episodic approvals towards ongoing, outcome-driven coverage models, shaping the landscape of pharmaceutical innovation incentives.

However, the development is not a guaranteed panacea; safety liabilities and lingering payer uncertainties could temper enthusiasm, and competing obesity treatments or disruptive modes of intervention (e.g., gene editing) may confound trajectories.

Competing interpretations may view oral GLP-1s as incremental convenience improvements rather than structural game changers; however, current evidence supports a broader ecosystem shift catalyzed by adherence, reimbursement, and safety dynamics.

Early Indicators to Monitor

- FDA approvals and expanded label updates for oral GLP-1 formulations addressing weight management

- Medicare and Medicaid policy developments related to GLP-1 reimbursement beyond 2027, including BALANCE Model adoption rates

- Launch and market share data for oral GLP-1 drugs, including generic entrant pricing strategies

- Post-market safety reports, particularly incidence trends of rare adverse events such as ischemic optic neuropathy linked to GLP-1s

- Capital deployment trends in pharmaceutical R&D focused on oral peptide formulations and digital adherence tools

Disconfirming Signals

- Regulatory rejection or severe labeling restrictions on oral GLP-1 safety grounds

- Failure of oral GLP-1 therapies to demonstrate superior or at least non-inferior adherence and weight maintenance compared to injectables

- Stable or expanding dominance of injectable programs with minimal oral adoption

- Lack of meaningful insurer reimbursement frameworks or policy extensions beyond the Medicare GLP-1 Bridge period

- Emergence of competing obesity paradigms (e.g., gene therapies) rendering oral GLP-1s obsolete

Strategic Questions

- How should capital be reallocated between injectable and oral obesity therapeutics within pharmaceutical R&D portfolios over the next five years?

- What regulatory and reimbursement models are most viable to incentivize long-term adherence to oral GLP-1s while managing safety and cost risks?

Keywords

Oral GLP-1; Weight Management; Obesity Therapeutics; Pharmaceutical Regulation; Medicare Reimbursement; Drug Safety Surveillance; Pharmaceutical Pricing; Digital Therapeutics

Bibliography

- Lilly's data, meanwhile, addresses a key concern for the broader GLP-1 class around the ability for patients to maintain weight loss after treatment with a high-dose incretin - a role that some industry watchers have suggested oral GLP-1s could fill. Fierce Pharma. Published 11/05/2023.

- The Ozempic oral pill, approved by the Food and Drug Administration (FDA), offers an option for adults with type 2 diabetes to manage blood sugar and cardiovascular risk alongside diet and exercise. Pharmaceutical Technology. Published 15/08/2023.

- Novo Nordisk's Wegovy pill is currently the only oral GLP-1 pill approved by the FDA for weight management, but Eli Lilly is expected to release its own-called orforglipron-later in 2026. Forbes. Published 31/03/2026.

- The weight-management drug Wegovy has become widely used and now comes in a convenient pill form - but recently, a study flagged that the popular medication may carry a risk of eye stroke, also called ischemic optic neuropathy (ION), which can cause rapid vision loss. Live Science. Published 23/02/2024.

- There is no clear path forward for GLP-1 coverage in Medicare after 2027 if the Medicare GLP-1 Bridge is not extended further and the BALANCE Model is not implemented. KFF. Published 02/04/2024.

- Canada has recently approved a generic version of Ozempic, which could undermine Novo Nordisk's pricing power considerably. Investing.com. Published 12/12/2023.